| Published: Date: Updated: |

The Bahamas Investor Magazine January 19, 2012 January 19, 2012 |

The domestic economic environment during 2011 has to be viewed in the context of a weaker than expected recovery in the global economy and less positive performance indicators for the US. However, initial indications are that the gradual improvement in the domestic economy was upheld through the latter half of the year, supported mainly by ongoing construction sector projects and more modest gains in the tourism sector.

Given the weakness in real sector activity, high unemployment persisted through 2011, according to the most recent Central Bank of The Bahamas figures, while inflationary pressures remained relatively benign over recent months, although impacted by the recent firming in global oil prices.

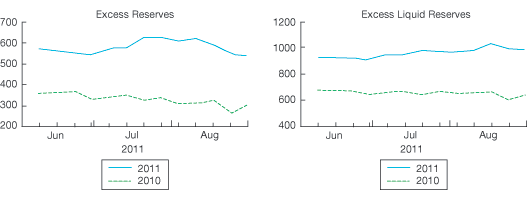

Against this backdrop the government continued to push forward with austerity measures put in place to reduce the budget deficit and stimulate economic growth. The fiscal situation for the early part of FY2011/2012 showed a contraction in the overall deficit, while monetary developments continued to feature high and stable levels of bank liquidity and external reserves (see charts), amid soft private sector demand.

The fiscal numbers presented in the 2011/2012 budget communication were greatly affected by revisions to the gross domestic product (GDP) estimates. The ratio of Recurrent Revenue to GDP is now significantly lower than previously estimated, with 2010/2011 estimates coming in at a “disappointing” $1,460 million, down from the forecast of $1,492 million, and putting the country even further away from the much-desired objective of 20 per cent of GDP.

Recurrent Expenditure in 2010/2011 is now estimated to be some $1,644 million, up $90 million from the previous budget forecast. Recurrent Deficit for fiscal 2010/2011 is now expected to be $184 million, up $122 million from the previous budget forecast, but down by $75 million from its level in 2009/2010.

Government Debt mid-way through 2011 is estimated as being $3.5 billion, or 44.9 per cent of GDP, a significant improvement from the expected level of 49.2 per cent. Capital Revenue was significantly bolstered in 2011, to the tune of $210 million, by the proceeds of the sale of 51 per cent of the government’s holdings in the Bahamas Telecommunications Company (BTC). This contributed to a significant decline in the GFS Deficit in 2010/2011 to $130 million, down by $97 million from the $227 million estimate presented in the previous year’s budget. The deficit will amount to 1.7 per cent of GDP, as compared to the projected level of 3 per cent.

With the new GDP numbers, the Bahamian economy is now estimated to have grown by a little over 1 per cent in real terms in 2010 to around $7.7 billion, following consecutive declines of 1.3 per cent and 5.4 per cent in 2008 and 2009, respectively. At press time, the International Monetary Fund (IMF) estimates that growth during 2011 will be nearer 1.3 per cent (see Figure 2) and predicts growth of around 2 per cent for 2012.

This modest recovery in the domestic economy was expected to be sustained over the remainder of 2011, according to Central Bank, although significant global headwinds could damper prospects for tourism sector recovery and constrain the growth momentum into 2012. Foreign investment-led projects, combined with public sector programmes, are anticipated to support the ongoing rebound in the construction sector and gradual improvement in associated labour market conditions. Given the volatility in international oil prices, modest firming in domestic inflation is forecasted over the near-term.

In the fiscal sector, efforts to secure an improvement in the overall deficit and slow the growth in the corresponding debt indicators hinge significantly on the strength and sustainability of the economic recovery, along with the success of the government’s efforts to enhance revenue collections.

On the monetary front, both bank liquidity and external reserves are poised to remain at elevated levels over the remainder of the year, although with some reduction towards the end of the year, in-line with the anticipated seasonal, though reduced, upturn in domestic demand. In the context of the mild growth scenario and limited employment prospects, banks’ credit quality indicators are expected to stay elevated; however, with capital at healthy levels, financial stability concerns remain muted.

Sidebar: Economic overview